Recall in the short-run, firms can either have economic loss, economic profit, or break-even.

In the long run, firms will always end up breaking even.

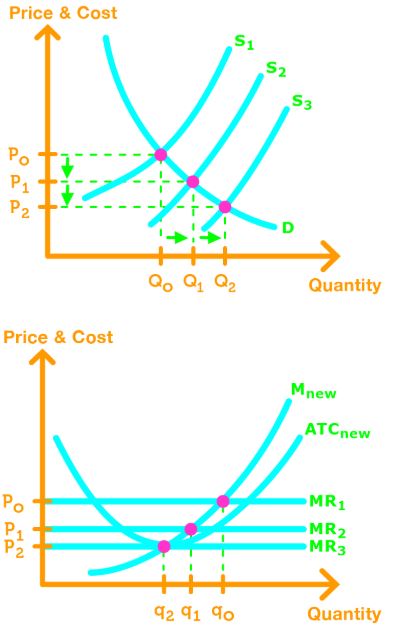

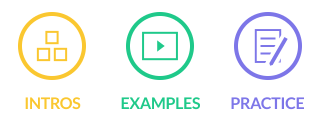

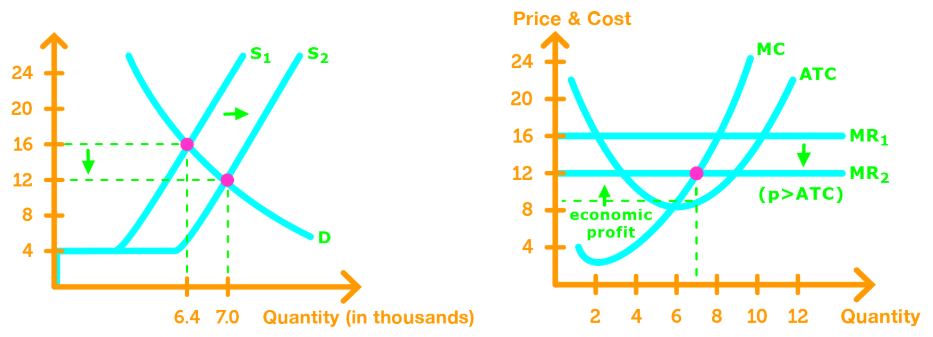

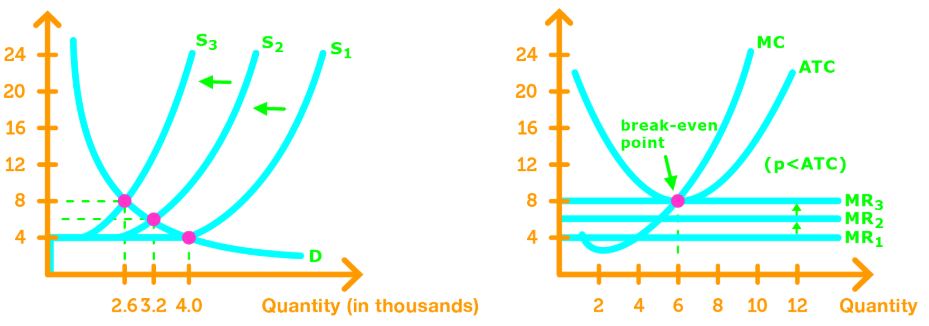

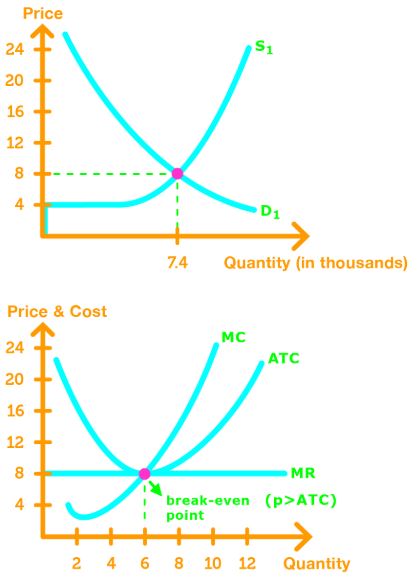

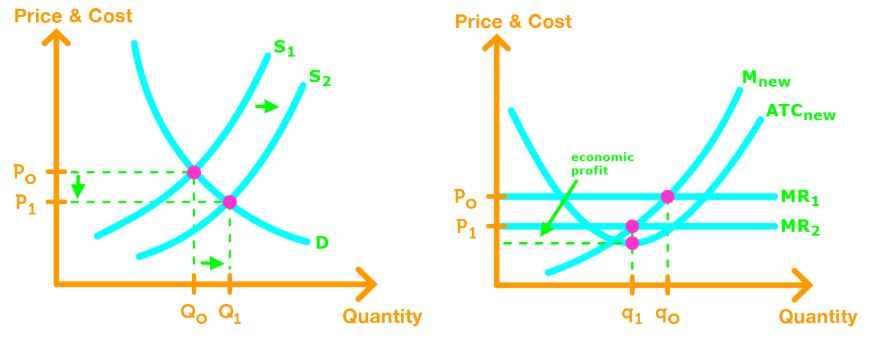

Entry: Firms will only enter the market if firms in the market are making economic profit (p > ATC).

When firms enter the market, they increase the supply, shifting the supply curve rightward. This causes the equilibrium price to decrease, which also causes the MR curve (p) to shift down.

The supply curve keeps shifting rightward until p = ATC In this case, the firms break even.

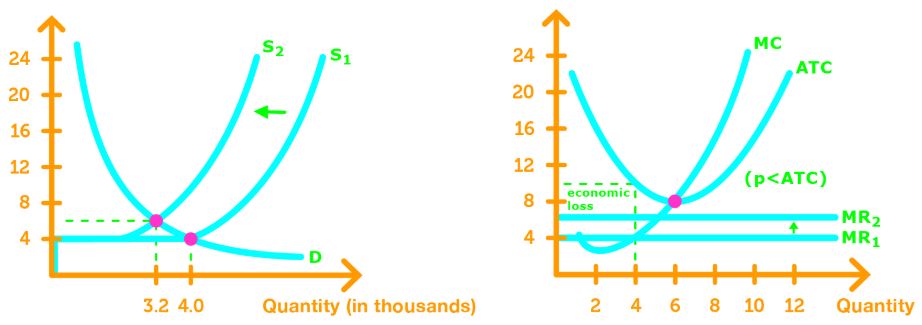

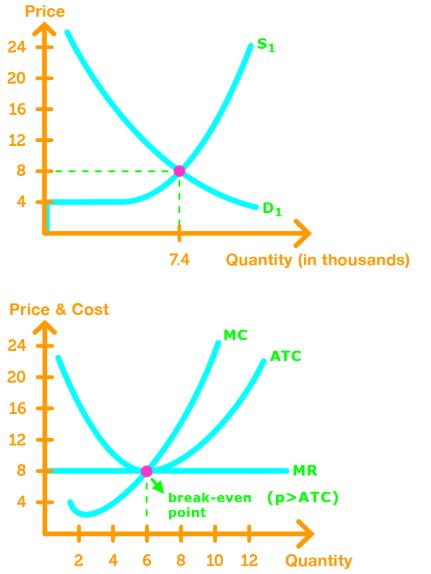

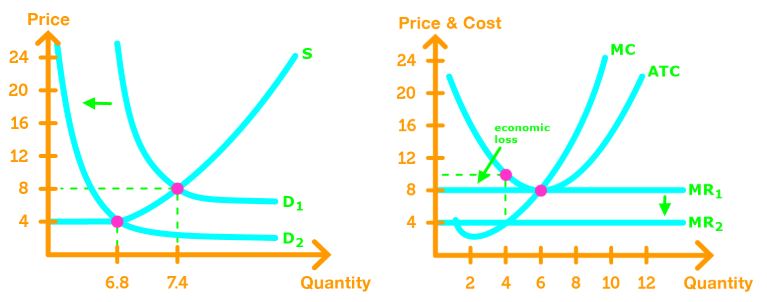

Exit: Firms will only exit the market if they are incurring economic loss (p < ATC).

When firms exit the market, the decrease the supply, shifting the supply curve leftward. This causes the equilibrium price to increase, which also causes the MR curve (p) to shift up.

The supply curve keeps shifting leftward until p = ATC. In this case, the firms again break even.

Long Run: Changes to Demand

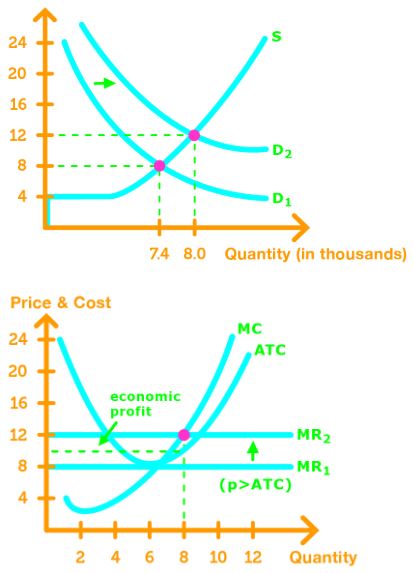

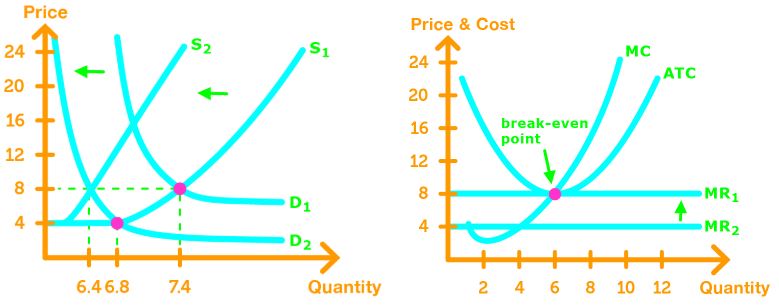

Increase in Demand: Suppose the firm’s profit is breaking even.

The increase in demand shifts the demand curve rightward, causing an increase to equilibrium price. This causes the MR curve (p) to shift up.

Firms will see that p > ATC, so there is an economic profit. This causes firms to enter the market, which will shift the supply curve rightward and decrease equilibrium price. Thus, the MR curve (p) shifts back down.

The MR curve shifts down until p > ATC. Hence, the firms will break-even.

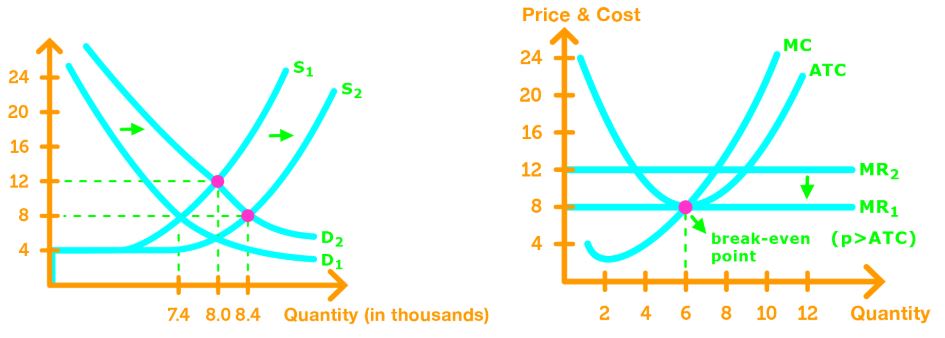

Decrease in Demand: Suppose the firm’s profit is breaking even.

The decrease in demand shifts the demand curve leftward, causing a decrease to equilibrium price. This causes the MR curve (p) to shift down.

Firms will see that p < ATC, so they will incur economic loss. This causes firms to exit the market, which shifts the supply curve leftward and increase equilibrium price. Thus, the MR curve (p) shifts back up.

The MR curve shifts up until p = ATC. Hence, the firms will break-even.

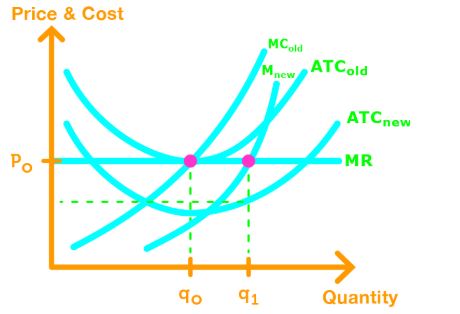

Long Run: Changes to Supply as Technology Advance

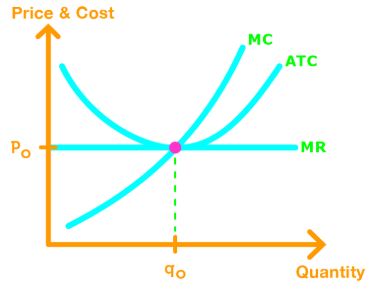

Decrease in Cost: Suppose the firm’s profit is breaking even.

Technology advances will shift the ATC curve and MC curve downward, causing firms to have economic profit.

This causes firms to enter the market, which will shift the supply curve rightward and decrease equilibrium price. This causes the MR curve (p) to shift down.

The MR curve will shift down until p = ATC. In this case, the firms will break-even.