Definition of Monopoly

Monopoly: a market with a single seller who sells a unique product that no other firms can produce.

A Monopoly is a market which has the following two features:

Barriers to Entry:

There are 3 types of barriers to entry:

Methods to Setting Prices to Monopoly:

In a monopoly, the firm can set its own prices. However, they also know that the amount of quantity produces changes the market price. There are two methods to setting prices to buyers:

Monopoly: a market with a single seller who sells a unique product that no other firms can produce.

A Monopoly is a market which has the following two features:

- No Close Substitute: If one or more firms can produce a close substitute, then the single seller will face competition from the producers of the substitute.

- Barrier to Entry: are constraints that prevent or makes it extremely difficult for new firms to enter the market.

Barriers to Entry:

There are 3 types of barriers to entry:

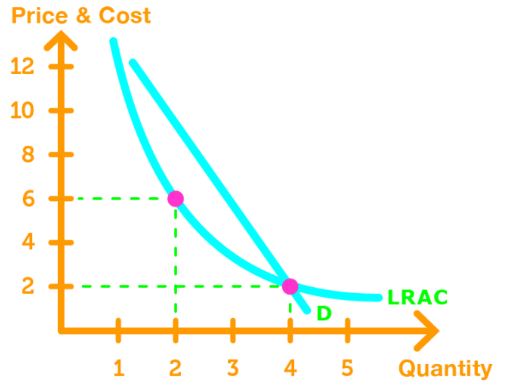

- Natural Barrier to Entry: Economies of Scale causes one firm to be able to supply the entire market at the lowest possible cost. A natural barrier to entry creates natural monopoly.

- Ownership Barrier to Entry:occurs when one firm owns a huge portion of a resource that is used to produce the good.

- Legal Barrier to Entry:a barrier where competition and entry are restricted by the granting of:

- Public franchise: exclusive right granted to a firm to supply a good or service

- Government license: controls entry into specific jobs, or industries

- Patent: exclusive right given to the inventor of a good

- Copyright: exclusive right given to an author or composer.

Methods to Setting Prices to Monopoly:

In a monopoly, the firm can set its own prices. However, they also know that the amount of quantity produces changes the market price. There are two methods to setting prices to buyers:

- Single-Price Monopoly: the firm sells each unit of output for the same price to all buyers.

- Price Discrimination: the firms sell their unit of output for difference prices to different buyers.

Note: When firms price discriminates, their motive is to charge the highest possible price for each unit sold to gain the most profit.