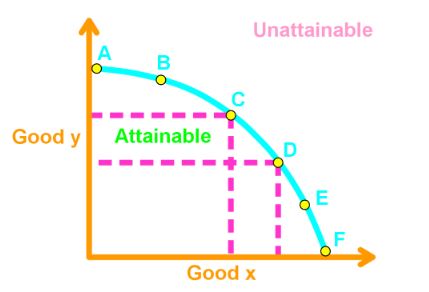

Production Possibilities Frontier

Key ideas to note in a PPF:

PPF represents all possible choices of production for a business, or an economy. The PPF shows the limits to the production of two specific goods, when given the available resources and technology.

Production Efficiency: Is achieved when the production of goods and services are at the lowest possible cost.

Key ideas to note in a PPF:

- There is always a tradeoff along the PPF. (Opportunity Cost)

- Points outside the curve are unattainable.

- We achieve production efficiency when the point is on the curve

- When a point is inside the curve, this is product inefficient.

Opportunity Cost: is the benefit, profit, or value of something that must be given up to acquire something else.

Note: Opportunity Cost is a ratio between the decrease in quantity of a good and an increase in quantity of another good along the PPF.