Perfect Competition is a market that has a lot of small firms which can produce a similar good for sale and profit.

No firm’s product is better than another firm. The goods are perfect substitutes.

For a market to have perfect competition, 4 conditions must apply:

- Many firms sell identical products to many buyers

- Firms find it easy to enter & exit the market

- Established firms have no advantage over new firms

- Buyers and sellers are well informed (everyone has full information)

Price Takers: a firm that cannot influence the market price due to the firm only selling a fraction of the market output.

Economic Profit & Revenue

The goal of a firm is to always maximize profit. To calculate profit, we take the revenue and subtract it by cost.

To maximize profit, we need to get the highest possible revenue with the lowest possible cost.

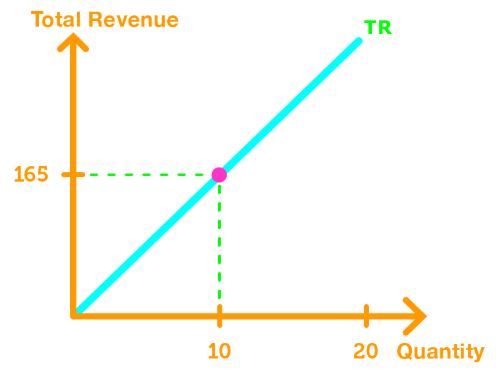

Total Revenue: is the price of it’s output multiplied by the number of units of output sold. In other words,

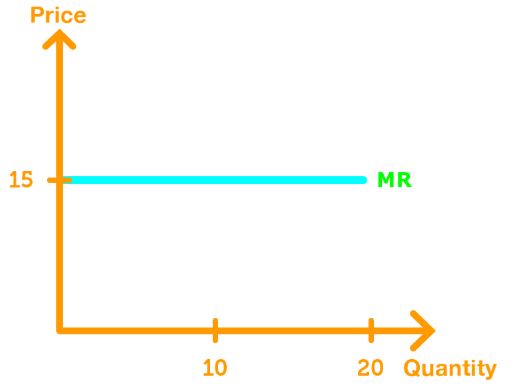

Marginal Revenue: is the additional revenue gained from a one-unit increase in quantity sold.

In perfect competition, the marginal revenue (demand curve for firm) is horizontal because firm’s have no influence on market price. So, they must sell all the products at the same price.

Decision of Firms

In a perfect competition, must decide on

- How to produce at the lowest cost

- How many quantities to produce

- Should the firm enter or exit the market